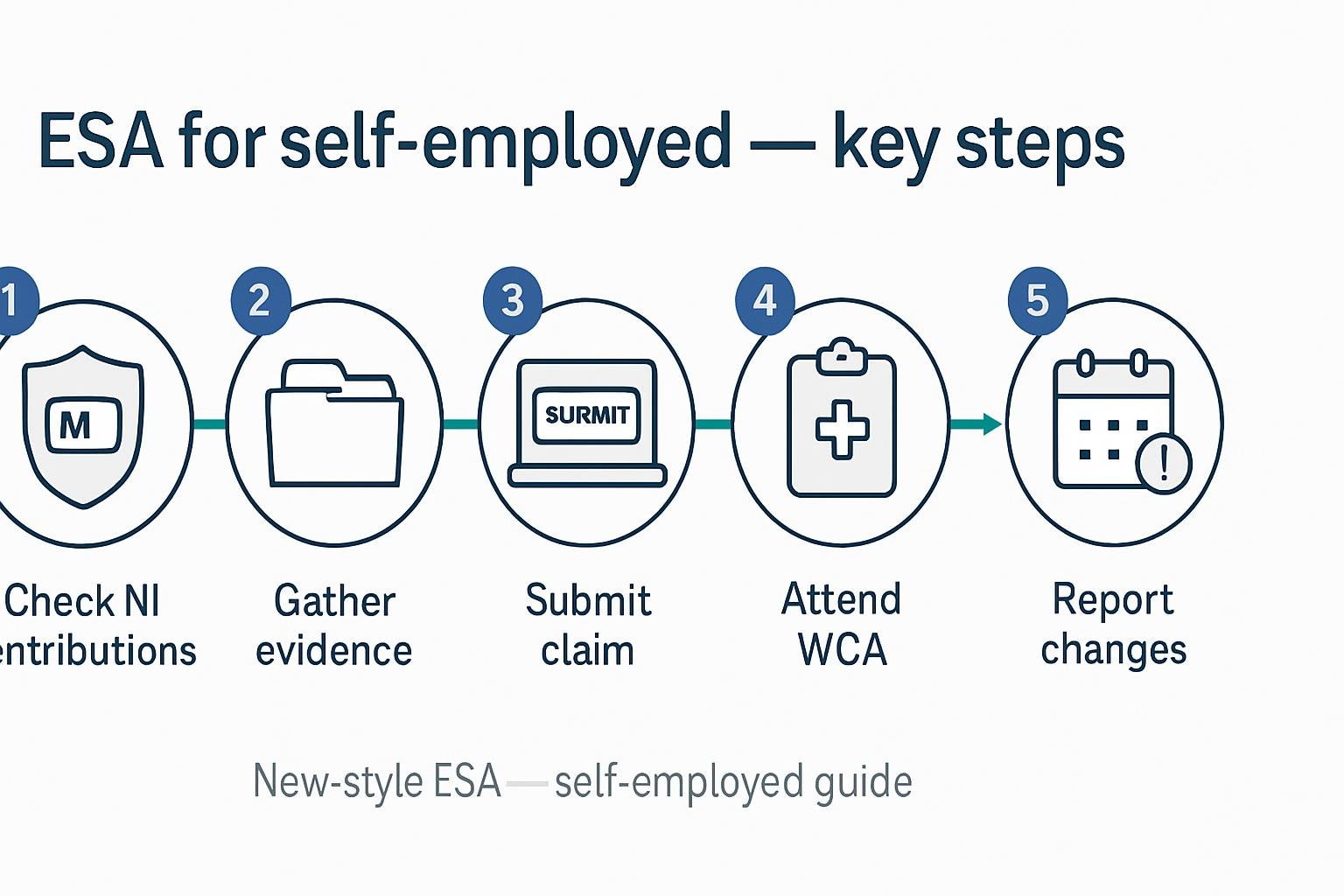

New Style Employment and Support Allowance (ESA) for self-employed

Published: 28 Jan 2026

Introduction

New-style Employment and Support Allowance (ESA) is a contribution-based benefit for people whose illness or disability affects their ability to work. For self-employed individuals, eligibility depends mainly on your National Insurance contribution history (particularly Class 2 contributions) and on how your health condition limits the tasks required by your trade. This article explains who can qualify, which National Insurance payments matter, how self-employment earnings are assessed (profit vs turnover), the role of fit notes and the Work Capability Assessment (WCA), how to make a claim and what evidence to provide, payment rules, reporting requirements, and how to challenge decisions — so self-employed claimants can apply correctly and secure the support they need.

Who can get New-style ESA

Reasons you may qualify

New-style Employment and Support Allowance (ESA) is a contribution-based benefit for people whose illness or disability affects their ability to work. You may qualify if you meet the contribution conditions (sufficient National Insurance record), are resident in the UK and have a health condition that limits your capability for work. For self-employed people, eligibility depends mainly on your Class 2 National Insurance contributions or recent Class 1 contributions from employed work. If you have paid sufficient contributions in the relevant qualifying years, you can claim contribution-based New-style ESA even if you no longer have paid employment.

Self-employed applicants should show that the health condition prevents them from carrying out the business activities that generate their profits. DWP looks at functional impact rather than the legal status of self-employment; if your illness prevents you from doing the core tasks of your trade, you can be eligible.

Eligibility for self-employed people

Contribution years and rules

To get contribution-based New-style ESA you normally need sufficient National Insurance contributions in the relevant tax years. The DWP test usually checks your NI record for the tax year before the claim and the previous year (so-called qualifying years). For many claimants this means proving you paid enough Class 1 (if recently employed) or Class 2 (if self-employed) contributions.

If you recently switched to self-employment, your entitlement may rely on previous employed NI payments. If your Class 2 record has gaps, you may be able to make voluntary Class 2 payments for previous years to fill those gaps — but only within HMRC time limits. Always check your National Insurance record on gov.uk and contact HMRC to correct or pay missing years before applying if possible.

Class 2 vs Class 4 NICs explained

For self-employed people it’s vital to know which NICs count:

- Class 2 NICs: a flat weekly/self-employed contribution that counts towards contribution-based benefits and the State Pension. Paying Class 2 helps meet the ESA contribution test.

- Class 4 NICs: a profit-based percentage payable through Self Assessment; these do not count as contributions for ESA entitlement.

Many new self-employed people are surprised that their Class 4 payments don’t help with benefit entitlement. If you have not paid Class 2 for some years, investigate voluntary Class 2 options through HMRC. Also check that HMRC’s records correctly reflect any Class 2 payments already made.

National Insurance conditions (Class 2/4) for eligibility

Class 2 vs Class 4 NICs explained

(Clarified for this section) DWP requires contributions that count — primarily Class 1 or Class 2. If you only paid Class 4, that alone will not usually qualify you. When preparing a claim, gather evidence of Class 2 payments or proof of recent employment with Class 1 contributions. If necessary, use HMRC services to request a National Insurance statement and correct errors before applying.

How National Insurance credits affect future state pension

When you’re on New-style ESA you may receive National Insurance credits for the period you cannot work. These credits protect your State Pension record by counting as qualifying years. For self-employed people, receiving credits while you’re unable to work helps avoid losing pension entitlement through missed contributions. Confirm with HMRC which credits will be recorded; keep copies of DWP letters that confirm credit periods.

When to apply (timing and claim start)

When to start the claim if newly self-employed

Apply for New-style ESA as soon as your condition prevents you from working normally. Delaying may push you past waiting periods for payments and can complicate evidence collection. If you just started self-employment, apply immediately when symptoms affect your ability to trade—DWP can consider both recent employment history and self-employment when assessing contributions. Early application helps secure any NI credits from the earliest date you stop working due to illness.

If you’re unsure whether you meet contribution rules, still start a claim and explain your contribution history — DWP can advise and may accept supporting evidence. Keep careful dates: the date you notify DWP often decides the start of entitlement and any backdating.

How to make a claim (online, phone, post)

Step-by-step online claim process

- Prepare documents: NI number, identity (passport/driving licence), Self Assessment details (SA302 or tax return), business bank statements, invoices, fit note.

- Go to gov.uk and search for New-style ESA. Use the official online service to begin the claim.

- Provide personal details, residence status, and an honest description of how your condition affects your work tasks.

- Indicate self-employment status and give profit figures or recent earnings as requested. Upload SA302 or equivalent profit & loss summaries where asked.

- Submit any initial medical evidence and note the requirement to attend a Work Capability Assessment (WCA) if invited.

- Take screenshots of confirmation pages and write down the claim reference.

Using the online service is fastest and allows attachments; it also records timestamps to support backdating requests or disputes.

Phone and postal claim tips

If you cannot use online services, call the DWP ESA claim line. Have your NI number and the same paperwork ready. For postal claims, request the ESA50 or relevant form pack (if provided) and return it by recorded post. Keep copies of all documents and a note of dates you posted items. When speaking to advisers, note names and reference numbers. If you have difficulty completing forms, local Citizens Advice or disability charities can help fill them in.

What evidence to provide (self-employment income records)

Documents checklist

Self-employed claimants should prepare:

- SA302 tax calculation pages or full Self Assessment tax returns for the last 1–3 years.

- Business accounts or simple profit & loss summaries showing turnover and allowable expenses.

- Business bank statements corresponding to the tax years claimed.

- Invoices, receipts, and contracts showing regular clients or one-off work.

- Proof of Class 2 NI payments and any voluntary contributions.

- Fit notes, clinic letters, hospital discharge summaries, and specialist reports.

- A written statement explaining how your condition affects specific business tasks (e.g., inability to lift, travel, concentrate for required periods).

- Any evidence of attempts to adapt work or get reasonable adjustments (assistive equipment, changed hours).

Organise these in date order and label them before uploading or posting. For seasonal businesses, include several years of records to show typical earnings patterns.

Fit note and capability for work assessment (Work Capability Assessment)

What a fit note shows and how to get one

A fit note (sick note) from your GP confirms your medical condition and whether you’re not fit for work or might be fit with adjustments. It’s not essential to have a fit note to claim ESA, but having recent, specific fit notes increases the chance of a successful WCA outcome. Ask your GP or treating clinician to describe specific functional limitations (e.g., cannot stand for >10 minutes, cannot lift >5 kg, needs frequent rest breaks).

If your GP won’t provide detailed function-based notes, request a referral for specialist letters or physiotherapy assessment that can add weight to your claim.

What the Work Capability Assessment looks at

The WCA is a points-based assessment that evaluates physical and mental functional descriptors across activities such as mobility, manual dexterity, communication, learning, and coping with social contact. The process can include a questionnaire, face-to-face or remote assessment with a health professional, and review of medical records.

Descriptors carry point values; reaching a threshold puts you in the Support Group (higher rate, no work-related activity requirement) or WRAG (work-related activity group), or a decision of “fit for work.” Prepare for the WCA by:

- Completing the medical questionnaire fully with examples.

- Submitting up-to-date medical evidence.

- Explaining how typical work tasks are affected (e.g., impact on drafting invoices, meeting clients, manual tasks).

- Bringing examples of daily routine limitations to the assessment.

If mobility or communication issues make attending difficult, request a home assessment and provide supporting evidence.

How self-employed earnings are assessed (profit vs turnover)

Profit calculation examples

DWP assesses earnings from self-employment as taxable profits (turnover minus allowable business expenses), not gross turnover. Use your Self Assessment figures (taxable profit) as primary evidence. Example:

- Turnover: £30,000

- Allowable expenses: £12,000

- Taxable profit: £18,000 — this profit figure is what DWP will consider for means-tested components and some overlaps with other benefits.

If you use cash accounting or have unusually high one-off costs, explain these clearly and include bank statements and invoices to show the pattern.

Seasonal income example

For seasonal work (e.g., tourism, agriculture), DWP may average earnings across recent years or ask for representative periods. Provide multiple years of accounts and a written explanation of seasonal cycles. For example, a landscaper may have most income April–September; show monthly bank inflows and invoices to demonstrate the typical trading cycle rather than a single anomalous year.

If your most recent year is unusually low due to illness, include previous years to present a typical earnings picture and explain circumstances for the low year.

Impact of fluctuating income and seasonal work

Seasonal income example

Fluctuating income affects both contribution records and current means assessments. If your profits vary widely, DWP aims to assess what constitutes your usual earnings. Provide:

- Profit & loss summaries for 3–5 years where possible,

- Bank statements,

- Contracts or correspondence indicating expected future work,

- Explanations of any sudden drops (e.g., loss of a major client) and supporting evidence.

A clear payment pattern and professional bookkeeping strengthen claims and reduce misunderstandings over MIF or other assessment rules when you also claim Universal Credit.

Interaction with Universal Credit and other benefits

How ESA and Universal Credit are assessed together

New-style contribution-based ESA is distinct from income-related ESA and Universal Credit. You can claim New-style ESA based on contributions and still claim Universal Credit for living costs if eligible, but the combination and calculation can be complex:

- If you receive contribution-based New-style ESA and also claim Universal Credit, the ESA amount may be ignored for the UC housing element or treated differently depending on local rules.

- For self-employed people on UC, the Minimum Income Floor (MIF) can assume a notional income for benefit calculation unless you qualify for the Start-Up Exemption (you’re newly self-employed and in first 12 months) or a Limited Capability for Work condition. Receiving New-style ESA for limited capability can exempt you from MIF.

- Always declare New-style ESA to UC and vice versa. Failure to report may cause overpayments.

Get advice if you’re moving between ESA and Universal Credit, as transitional rules, tapering, and work allowances can affect net income.

For detailed guidance on how Universal Credit treats self‑employment (Minimum Income Floor, Start‑Up Exemption and reporting earnings) and how that can interact with an ESA claim, read: https://ukbenefitsguide.online/universal-credit-for-self-employed-guide-uk/

Receiving National Insurance credits while claiming

How National Insurance credits affect future state pension

When claiming contribution-based ESA, you may be awarded National Insurance credits for the claim period. These credits count as qualifying years for the State Pension and help maintain your NI record. For self-employed claimants who might otherwise miss Class 2 payments, ESA credits can protect pension entitlement. Check entitlement letters from DWP and confirm with HMRC that credits are recorded. Keep copies of DWP confirmations as proof when correcting HMRC records.

Payment amounts and how they’re calculated

Example payment calculations

New-style ESA contribution-based rates are fixed weekly amounts determined by gov.uk. The payment you receive depends on your age and whether you are placed in the Support Group or WRAG. While exact figures change with government updates, a worked example approach helps readers:

- Example: A claimant in WRAG receives the standard weekly rate for their group; if they start some paid work, earnings above permitted amounts can reduce ESA.

- If you have other earnings from self-employment, DWP may apply rules to offset ESA payments; declare earnings to avoid overpayments.

When publishing, always reference current gov.uk rates and update articles yearly (e.g., “rates for 2026”).

1. “Claiming support for your health is not giving up — it’s protecting your future business.” 2. “Your National Insurance record is part of your safety net; check it before you need it.” 3. “Good records today mean fairer decisions tomorrow — keep invoices, bank statements and medical notes.” 4. “A clear fit note and honest examples of daily limits make all the difference at the WCA.” 5. “Appeal if necessary — many decisions change after new evidence or a careful review.”M AMIR

When payments start and payment schedule

Payment timing and delays

ESA payments usually start after processing your claim and completing the necessary assessments. There can be delays due to scheduling the WCA or awaiting medical evidence. Typical sequence:

- Initial claim and evidence submission.

- Assessment phase (may include ESA assessment period).

- WCA appointment and report.

- Decision and payment start.

If payments are delayed, applicants can ask for an advance (an upfront payment) or apply for local welfare assistance for urgent needs. Keep proof of submission dates to support any backdating or hardship requests.

Reporting changes in circumstances (income, hours worked)

How and when to report income increases

You must report changes such as increased profits, start/stop of trading, changes of business hours, or returning to work. Report immediately via the DWP online account, phone line, or form. Specifically:

- Report any income above specified thresholds.

- Report changes in medical condition or return to work.

- Report changes in household composition affecting means-tested benefits.

Timely reporting prevents overpayments and sanctions; maintain monthly bookkeeping to report accurate figures.

Effect of Business Support payments or grants on claim

Which grants/countable payments affect ESA

Some business grants or support payments may count as income for ESA or deduction calculations. Small emergency grants or business rate relief might or might not be disregarded depending on type. Provide:

- Evidence of grant terms,

- Copies of grant letters,

- Advice to seek confirmation from DWP or Citizens Advice about whether a specific payment is counted.

Document all grants received and include them when requested by DWP.

How to report self-employment income during claim

How to fill in income sections on ESA forms

When DWP asks for income details, use taxable profit figures from Self Assessment or summarized monthly profit. Steps:

- Use SA302 or profit & loss to calculate weekly or monthly profit.

- Break annual profit into weekly/monthly average as requested.

- Explain any irregular large items (asset sales, one-off grants) and provide supporting evidence.

- Upload bank statements to corroborate declared figures.

Accuracy matters — misreporting can lead to penalty, overpayment, or claim failure.

Claiming ESA while registering as self-employed for the first time

Steps if you start a business while claiming

If you start trading while already claiming ESA:

- Notify DWP immediately with the date you start trading and expected earnings.

- Register for Self Assessment and Class 2 NI as soon as possible.

- Keep detailed records of start-up losses, initial investments, and projected income.

- DWP will assess how the new trade affects ESA; small start-up losses may not remove entitlement, but declared profits will be considered.

- Consider applying for Start-Up Exemption on UC if you are on Universal Credit as well.

Being proactive and transparent with DWP helps avoid sudden sanctions or overpayment recovery.

Voluntary Class 2 NICs to meet contribution conditions

How to pay voluntary Class 2 NICs and when it helps

If you have gaps in your National Insurance record and need to meet ESA contribution tests, you may be able to pay voluntary Class 2 NICs for past years. Steps:

- Check your NI record on gov.uk and identify missing years.

- Contact HMRC to see which years are eligible for voluntary payment (deadlines apply).

- Use HMRC’s online service to request to pay and make the payment.

- Keep receipts and confirm with HMRC that the payment counts for benefit entitlement.

Voluntary payments can be cost-effective if they secure contribution-based ESA or protect State Pension years.

How to challenge a decision (mandatory reconsideration, appeal)

Mandatory reconsideration and tribunal steps

If your claim is refused or you disagree with a WCA outcome:

- Request a Mandatory Reconsideration (MR) within the time limit stated on the decision letter (normally one month).

- Provide any new medical evidence or corrections to factual errors.

- If MR upholds the decision, you can appeal to an independent tribunal — attach full evidence, WCA report, and medical records.

- Consider getting an adviser (Citizens Advice, welfare rights officer, or specialist solicitors) to help prepare submissions.

Always keep copies of all correspondence and note deadlines. Timeliness and fresh medical evidence significantly help appeals.

Accessing extra help while waiting for decision (advance payments, hardship)

How to apply for advance payments and local hardship help

If you face financial hardship while waiting:

- Apply to DWP for an advance payment (repayable from future ESA) or request hardship payments if eligible.

- Contact local councils for discretionary local welfare assistance or crisis grants.

- Approach food banks, charitable trusts, and Citizens Advice for immediate support.

Document your financial situation (bank statements, bills, rent arrears) to speed up applications for emergency help.

You can also check local crisis grants and bursaries for students which may provide immediate one‑off help while you wait for ESA decisions — useful if you’re studying and self‑employed or have short‑term cash needs. See: https://ukbenefitsguide.online/crisis-grants-bursaries-students-uk/

Online and local help resources (Citizens Advice, gov.uk links)

Key gov.uk and Citizens Advice pages to bookmark

Essential resources:

- gov.uk New-style ESA pages (claiming, rates, WCA guidance)

- Citizens Advice guides on ESA and self-employment

- HMRC pages for Self Assessment and voluntary Class 2 NICs

- Local jobcentre plus offices and disability charities for practical support Bookmark and cite these pages; link to them in your article for credibility and up-to-date data.

Record-keeping checklist for self-employed ESA claimants

Minimum records to keep and retention period

Keep:

- Self Assessment tax returns and SA302s,

- Profit & loss summaries, invoices, receipts,

- Business bank statements,

- Contracts and client correspondence,

- Fit notes, hospital letters, clinic correspondence,

- DWP letters and claim references. Retention: keep tax records for at least 5 years after the relevant tax year (HMRC guideline) and longer if DWP requests older evidence.

Organise records chronologically and keep digital copies for safe backup.

Common reasons for ESA claim rejection and how to avoid them

Top 10 common rejection reasons

- Insufficient National Insurance contributions — check NI record and consider voluntary Class 2.

- Weak medical evidence — obtain clear, function-focused GP/specialist reports.

- Submitting turnover instead of profit — use taxable profit figures.

- Incomplete forms — double-check all answers and sign forms.

- Missing supporting documents — attach SA302, bank statements, fit notes.

- Not reporting start/stop of self-employment — notify DWP immediately.

- Failure to attend WCA or provide correct contact details — rearrange promptly and provide evidence for non-attendance.

- Not explaining seasonal income patterns — include multi-year accounts and written explanation.

- Misunderstanding interaction with Universal Credit — get tailored advice when claiming both.

FAQs

You can claim if your illness or disability limits your ability to do the core tasks of your trade and you meet the contribution test (usually sufficient Class 2 NI or recent Class 1 contributions).

No. Class 4 NICs do not count toward contribution-based ESA entitlement; Class 2 (or recent Class 1) contributions are the ones that matter.

DWP uses taxable profit (turnover minus allowable expenses) as the basis. For irregular or seasonal incomes they may average profits over recent years or ask for representative evidence.

Typical documents: SA302 or Self Assessment returns, profit & loss summaries, business bank statements, invoices/contracts, proof of Class 2 payments, fit notes and medical reports outlining functional limitations.

Request a Mandatory Reconsideration within the time limit, submit new medical evidence if available, and if still refused you can appeal to a tribunal. Seek help from Citizens Advice or a benefits adviser.

Conclusion

New‑style ESA can provide vital financial support for self‑employed people whose health prevents them from working. The key to a successful claim is demonstrating that your condition affects the specific tasks of your business, meeting the National Insurance contribution test (mainly Class 2 or recent Class 1), and submitting clear, well‑organised evidence—SA302s, bank statements, fit notes and medical records. Understand how earnings are assessed (use taxable profit, not turnover), report changes promptly, and prepare for the Work Capability Assessment. If refused, use mandatory reconsideration and appeal routes and get specialist advice. Keeping accurate records and seeking local support (Citizens Advice, HMRC, DWP) will improve your chances of securing the right entitlement.

- Be Respectful

- Stay Relevant

- Stay Positive

- True Feedback

- Encourage Discussion

- Avoid Spamming

- No Fake News

- Don't Copy-Paste

- No Personal Attacks

- Be Respectful

- Stay Relevant

- Stay Positive

- True Feedback

- Encourage Discussion

- Avoid Spamming

- No Fake News

- Don't Copy-Paste

- No Personal Attacks